Over the past decade, climate change discourse has shifted from optional to regulatory, emphasizing the need for net-zero emissions and aligning with IPCC's 1.5-degree Celsius target. Nature-based solutions are crucial in this effort, offering significant carbon reduction potential. Research by the World Economic Forum (2021) (1) suggests they could deliver about one-third of the needed emissions cuts by 2030, equivalent to roughly 7 Gigatons of carbon removal, and at a lower cost than alternative methods

Reflecting on 2023

Overview

In 2023, the Voluntary Carbon Market (VCM) encountered challenges despite record issuance and high prices. Criticism regarding integrity and transparency dampened achievements. Concerns over project integrity, offsetting claims, and the market's role in the Paris Agreement's Article 6 led to cautious buyer and investor behavior. Gloomy investor sentiment persisted due to global monetary policy tightening and increased capital costs.

Key Developments

Here are the key global and national developments of Voluntary Carbon Markets for the year of 2023.

Global Developments

New REDD+ Methodology

Verra unveiled its long-awaited REDD+ methodology (VM0048) on November 27, 2023, targeting over-crediting issues in avoided deforestation projects. Developed in 2020, this methodology addresses concerns regarding baseline, leakage, and co-benefits, enhancing project integrity and potentially impacting market dynamics by stimulating buyer interest and increasing investments in global forest protection efforts. (7)

Regulation of Company Claims & Alternatives Introduced

The EU banned misleading green claims reliant on carbon offsets, effective by 2026, aiming to ensure accuracy in environmental messaging. Only sustainability labels endorsed by approved certification schemes will be permitted within the bloc. Additionally, VCMI and ICVCM collaborated to establish comprehensive guidelines ensuring integrity across Voluntary Carbon Markets (VCMs), introducing standards for carbon projects and advising companies on carbon credit usage and communication. (2)

VCMI enhanced its Claims Code with an MRA Framework and Carbon Integrity Claims branding. It introduced the beta version of the 'Scope 3 Flexibility'(3) Claim to address scope 3 emissions responsibly.

Advancements in Sustainability Accounting and Disclosure

Efforts to enhance transparency and credibility in voluntary carbon markets continued in 2023:

1) The International Sustainability Standards Board (ISSB) released IFRS S1 and IFRS S2, aligning with TCFD recommendations and enhancing transparency in sustainability reporting. (4)

2) Despite the dissolution of the Task Force on Climate-Related Financial Disclosures (TCFD), companies are still obligated to disclose TCFD-related information, overseen by the International Financial Reporting Standards (IFRS). (5)

3) The European Commission adopted the European Sustainability Reporting Standards (ESRS) for companies under the Corporate Sustainability Reporting Directive (CSRD), ensuring interoperability with global standards and reducing duplicate reporting. (6)

COP28: Initiatives & Article 6 Negotiations

The year's pivotal climate event saw a blend of successes and hurdles. While carbon market talks remained uncertain, advancements in Article 6 negotiations signaled positive momentum amid ongoing uncertainties, with many issues slated for resolution in the next COP.

LEAF coalition: Agreements between Costa Rica and Ghana to supply forest carbon credits to the LEAF coalition promise high-quality REDD credits in the market. (8)

“End to End” Integrity Framework: VCMI, in partnership with SBTi, GHG Protocol, and ICVCM, introduced a robust integrity framework at COP28, garnering support from leading corporations like Salesforce and Natura. These standards aim to elevate corporate climate action, aligning with science-based emissions targets. (9)

Collaboration to Strengthen Carbon Crediting Standards: Major carbon crediting standards, including ACR, ART, CAR, GCC, GS, and VCS, joined forces to enhance transparency and consistency in carbon markets. The initiative focuses on sharing best practices, ensuring community benefits, and increasing finance flow to developing nations, aiming for alignment with ICVCM's Core Carbon Principles. (10)

Article 6: The emphasis on the global stocktake under the COP presidency resulted in limited progress on the two Article 6 market mechanisms: Cooperative Approaches and Article 6.4 Mechanism. No decisions were made, hindering the advancement of project activities and the flow of carbon finance from the Global North to the Global South.

COP28 saw both ups and downs, but it marked a positive year for global carbon markets. Several nations advanced regulations and legislation to facilitate carbon credit trading in 2023, integrating carbon markets into their economies to address the urgency of the climate crisis

National Developments

In 2023, India introduced several initiatives in carbon markets and sustainability, signaling a positive start.

Carbon Credit Trading Scheme (CCTS): The CCTS, established under the Energy Conservation Act, 2001, sets GHG reduction targets for sectors, aiming to create a regulated carbon credit trading market. Administered by BEE and regulated by CERC, it awaits detailed specifications for full implementation. The compliance market is set to launch officially in 2026, covering sectors such as oil, gas, steel, and aluminum.

Green Credit Programme: Launched on October 13, 2023, this program incentivizes environmental actions through market-based mechanisms, focusing initially on water conservation and afforestation. Administered by the Indian Council of Forestry Research and Education (ICFRE), the program facilitates project registration, verification, and issuance of tradable Green Credit certificates via a digital platform.

Now, let's shift our focus from updates in global and national policies to insights from other prominent market participants. We'll delve into the noteworthy developments they've encountered throughout the year.

Major Nature-Based Solutions Collaborations & Transactions of 2023

In 2023, significant collaborations and transactions shaped the landscape of Nature-Based Solutions (NBS) initiatives, with corporations investing in various projects and establishing funds to support such efforts. Here are the key highlights:

Meta partnered with Aspiration to pre-order 6.75 Mt of carbon removal credits from diverse ecosystem restoration projects, including reforestation and sustainable agriculture. (15)

Mitsui invested in RRG Nature Based Solutions to advance regenerative agriculture in the US, blending agricultural expertise with innovative solutions. (16)

Microsoft secured a major deal with Mombak for up to 1.5 million carbon removal credits from Amazon reforestation, aligning with its carbon negativity goals. (17)

Amazon initiated a $3 million investment in nature-based projects in India as part of a $15 million fund for the Asia Pacific, including support for the "Wild Carbon" program. (18)

In 2023, Apple expanded the Restore Fund with Climate Asset Management, committing up to $200 million for nature-forward agriculture and ecosystem restoration. (19)

Lombard Odier Investment Managers (LOIM) collaborated with Systemiq to launch holistiQ Investment Partners, focusing on a net-zero and nature-positive economy. (20)

Global NGOs formed the SCeNe Coalition to deliver Nature-based Climate Solutions in Southeast Asia, promoting high-quality NbS initiatives. (21)

Ardian and aDryada introduced Averrhoa Nature-Based Solutions, deploying 1.5 billion euros for large-scale projects aligned with climate and biodiversity goals. (22)

While these developments mark significant progress, further analysis of demand and supply metrics will provide insights into market reactions.

Analysis

In 2023, the Voluntary Carbon Market (VCM) faced challenges despite achievements like record issuance and high valuations. Concerns grew over integrity and transparency. Despite this, the VCM remained resilient and operational. Now, let's explore these dynamics in detail.

VCM Demand & Supply Dynamics

Issuances

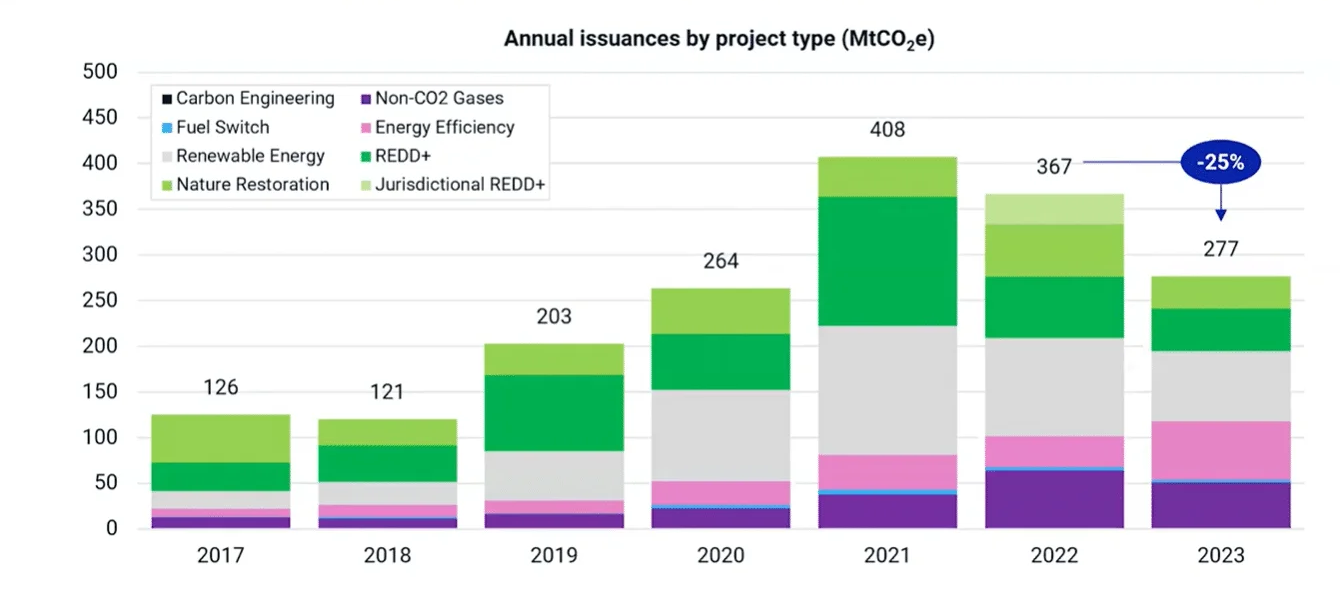

In 2023, credit issuances dropped by 25% compared to the previous year, marking a three-year low. **This decline was mainly due to reduced issuance from nature-based and renewable energy projects, hitting their lowest levels in five and four years, respectively.** One possible reason for this trend is the ongoing decrease in global credit prices, leading project developers to delay pre-issuance verification expenses.

Graph 1: Annual Issuances in 2023 (Source: MSCI) (12)

Conversely, energy efficiency projects were the sole major type to witness an increase in credit supply, doubling in volume compared to 2022. This surge was largely fueled by cookstove projects.

Retirements

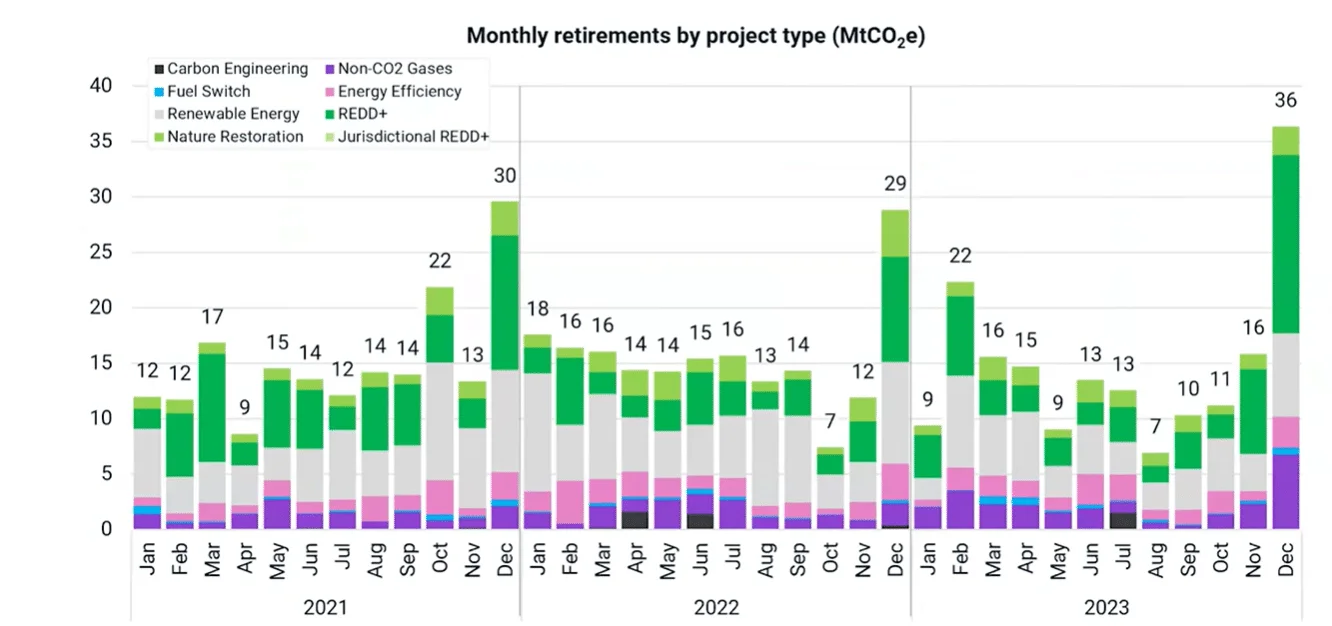

In Q4 2023, retirements surged, marking the second-highest quarter on record. January 2024 continued this trend, potentially surpassing the previous January's retirements. December 2023 set a new monthly record with 36 megatons retired, indicating sustained end-use of carbon credits despite announcements of buyer withdrawals. Buyers are recalibrating portfolios, considering environmental risks, and retiring previously acquired credits.

Graph 2: 2023 Monthly Retirements (Source: MSCI)(12)

In 2023, four sectors dominated retirements, comprising 75% of the total. The Fossil Fuels sector led with 37%, driven by Shell. Manufacturing (14%) and services (13%) followed closely. Despite a decline, Transportation (11%) remained in the top four, with Delta Air Lines and EasyJet reducing market presence. Overall, market concentration decreased, with the top 10 buyers (including Shell, Volkswagen, Takeda, Terpel, Yamato Group, Primax, Highland Fairview, Ecopetrol, Biomax, and DPD) representing 23% of retirements, down from 28% in 2022.

NBS Demand & Supply Dynamics

Nature-based solutions (NBS) play a crucial role in carbon credit supply due to their significant mitigation potential and various benefits. They also offer cost-efficient removal credits, which attract buyers.

Issuance

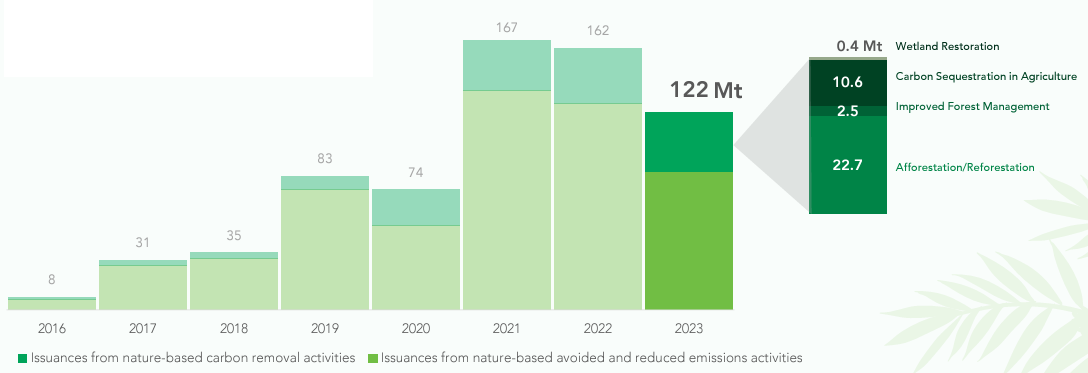

In 2023, issuance levels of NBS removal credits rose by 7%, reaching 36 Mt, representing over 10% of total annual issuances for the first time. The issuance from NBS credits was predominantly composed of Afforestation /Reforestation, accounting for 22.7 Mt, followed by Carbon Sequestration in Agriculture at 10.6 Mt, Improved Forest Management at 2.5 Mt, and Wetland Restoration at 0.4 Mt.

Graph 3: 2023 NBS Issuance (Source: Climate Focus)(13)

Despite a decline in issuances from avoided and reduced emissions credits from NBS, the interest in NBS carbon removal credits surged, partly driven by Science Based Targets initiative guidance. Criticism of certain REDD+ methodologies may have also contributed to this trend, leading buyers to prioritize removal credits to avoid reputational risks. Furthermore, a significant portion of issuances from nature-based projects in 2023 relate to newer vintages, indicating a shift away from older carbon credits.

Retirement

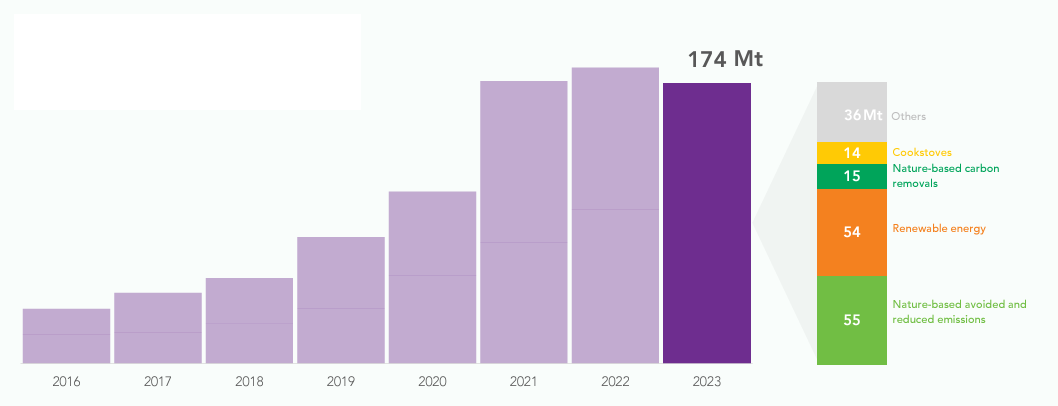

Nature-based avoided and reduced emissions projects take the lead, with 55 million credits retired, marking a 5% increase from 2022. Additionally, nature-based removals account for 8% of total retirement, totaling 15 Mt.

Graph 4: 2023 Retirement (Source: Climate Focus)(13)

A total of 174 million credits were retired, matching the volumes of the previous two years (183 Mt in 2022). These retirements accounted for nearly 20% of all historical retirements in the VCM. The weighted average credit age (vintage) for 2023 is approximately 5 to 6 years old, consistent with the trends observed in the two previous years.

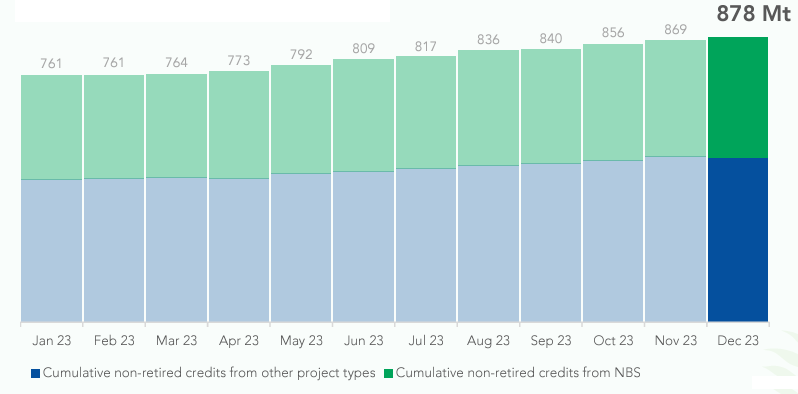

Open Volume

In 2023, non-retired carbon credits reached 878 Mt, with around one-third attributed to NBS credits. This surge in stockpiles, common in commodity markets, typically lowers prices. The remaining increase came from cookstoves and renewable energy projects.

Graph 5: 2023 Open Volume (Source: Climate Focus)(13)

It's worth noting that nearly one-fifth of the existing stockpile of non-retired carbon credits relates to pre-2016 vintages, which are becoming increasingly less appealing to buyers. These "legacy" credits are often considered of inferior quality, flooding the market and undermining its environmental credibility.

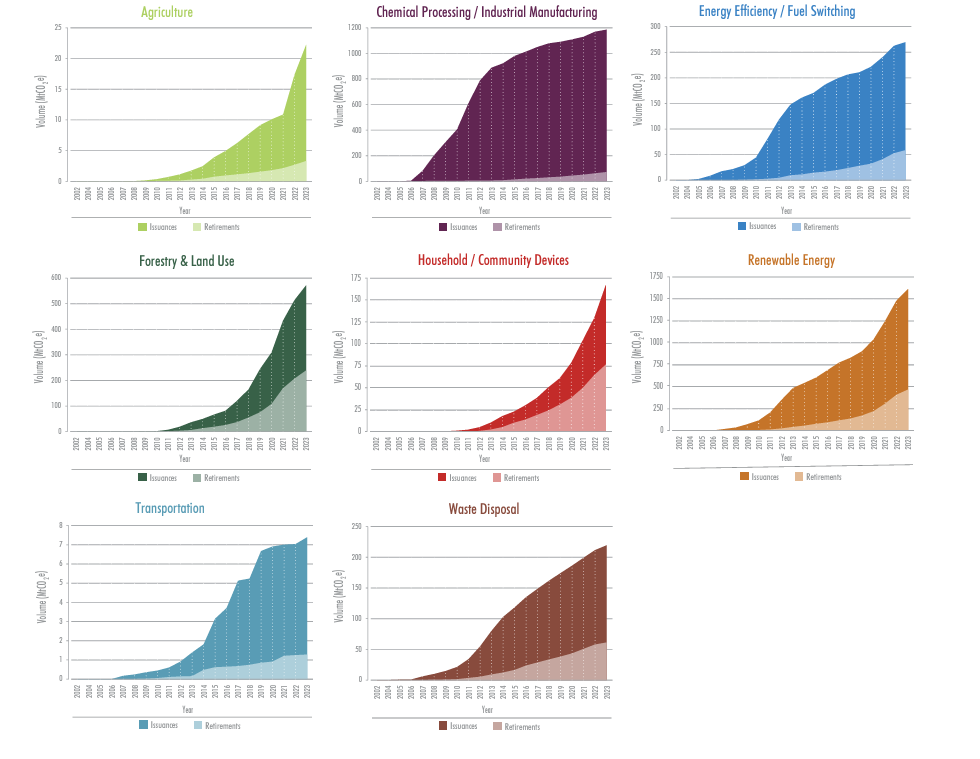

Graph 6: Cumulative Issuances and Retirements from 2002 to 2023 (Source: Ecosystem Marketplace) (14)

Agriculture, Forestry & Land Use project issuances surged, particularly in 2021 for Agriculture and 2020 for Forestry & Land Use. However, retirements for Agriculture credits lag, and while Forestry retirements increased in 2020, they haven't kept pace with issuances. This gap leads to a growing number of non-retired credits yearly, as shown in Graph 5.

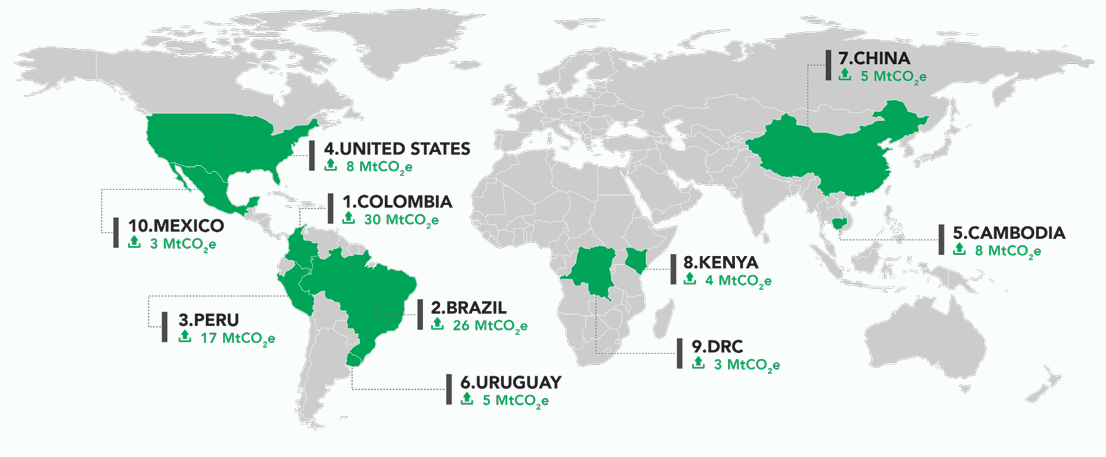

Top Suppliers of Nature-Based Solutions

In 2023, the majority of nature-based project supplies came from a few countries, with the top ten nations contributing nearly 90% (109 Mt) of the total. Colombia, Brazil, and Peru were the primary contributors, collectively representing about two-thirds of all issuances.

Graph 7: NBS Suppliers (Source: Climate Focus)(13)

Colombia led with 30 Mt, partly due to increased certification under the Cercarbono standard. This concentration is driven by the substantial scale of nature-based interventions, averaging nearly 0.5 Mt per project annually, contrasting with the more diverse landscape of supplier countries for non-nature-based projects, averaging just over 0.1 Mt per project.

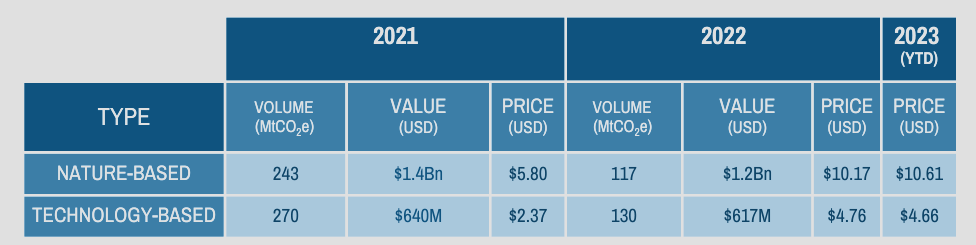

Price

In recent years, we've observed a significant price gap between nature-based solutions (NBS) credits and technology-based credits within the Voluntary Carbon Market (VCM). Despite similar volumes for both types of credits in 2021 and 2022, NBS credits commanded more than double the prices. Preliminary data for 2023 suggests an even greater premium for NBS credits.

Table 1: YOY Price, Volume, and Value comparison between Nature Based and Technology Based (Source: Ecosystem Marketplace) (14)

These credits primarily include REDD+ projects along with other types like Sustainable Agriculture Land Management, Afforestation/ Reforestation/ Revegetation (ARR), Agroforestry, and Blue Carbon. While prices for Agriculture and Forestry and Land Use credits continue to rise, the price increases for categories like Energy Efficiency and Renewable Energy seen in 2022 are now tapering off.

Table 2: YOY Price, Volume, and Value comparison between SDG and No SDG projects (Source: Ecosystem Marketplace) (14)

Carbon crediting standards increasingly require the declaration of Sustainable Development Goals (SDGs) during project registration to comply with CORSIA eligibility. SDGs cover objectives like clean water, affordable clean energy, and sustainable cities. In 2022, credits from SDG-aligned projects held an 86% premium over those not targeting SDGs, up from 57% in 2021.

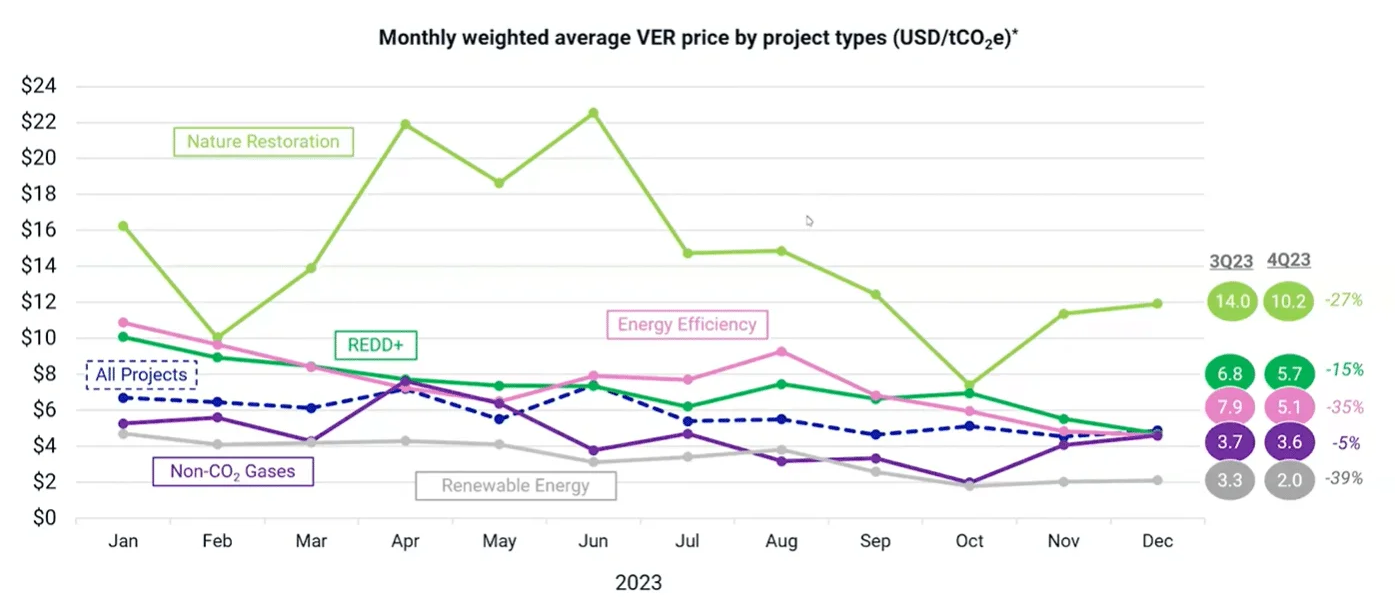

Graph 8: MOM Price by Project Type in 2023 (Source: MSCI)(12)

In 2023, prices fell across all project types, with renewable energy projects seeing the sharpest decline (39%), while REDD+ projects saw a relatively modest decrease (15%). Despite the scrutiny, energy efficiency and REDD+ projects maintained weaker prices. Towards the year's end, nature restoration and non-CO2 gas projects rebounded. However, energy efficiency, REDD+, and non-CO2 gases projects ended the year at similar price levels, suggesting a lack of market differentiation and a weak market environment.

Conclusion

The Voluntary Carbon Market (VCM) of 2023 presented significant challenges amidst its achievements, marked by record issuances and high prices. Criticism surrounding integrity and transparency overshadowed the market's progress. However, the VCM remained resilient, adapting to evolving demands and global policy changes.

Despite a decline in issuances from nature-based and renewable energy projects, their importance in the carbon market continued to grow. Notably, nature-based solutions (NBS) credits gained traction, driven by their significant mitigation potential and cost-efficiency. Projects like REDD+ witnessed increased issuance, albeit with some criticism regarding methodology.

The year also saw major global and national developments, including the unveiling of new REDD+ methodologies, enhanced sustainability accounting, and disclosure standards, and significant progress in Article 6 negotiations.

The market also witnessed notable collaborations and transactions, with corporations investing heavily in nature-based projects. Price dynamics continued to favor NBS credits, with preliminary data for 2023 suggesting an even greater premium. Despite challenges, the VCM demonstrated resilience and adaptability, reflecting its crucial role in combating climate change.

The year 2023 may have presented significant hurdles, but it also highlighted the importance of nature-based solutions in addressing the urgent climate crisis. As we move forward, it's clear that collaboration, transparency, and innovation will be essential in navigating the complexities of carbon markets and ensuring a sustainable future.

References

1) Nature and Net Zero by WEF & Mckinsey

2) VCMI & ICVCM Collaborative Effort

3) VCMI Carbon Integrity & Scope 3 Flexibility Claims

4) ISSB issues inaugural global sustainability disclosure standards

5) TCFD Disbanded

6) The Commission adopts the European Sustainability Reporting Standards

7) Verra’s New REDD Methodology

8) Costa Rica and Ghana to supply forest carbon credits to the LEAF coalition

9) End-to-End integrity framework

10) Independent Crediting Programmes Announce Collaboration to Increase the Positive Impact of Carbon Markets

11) Base Carbon’s Rwanda Cookstove Project Receives Corresponding Adjustment Label by Verra

12) 2023 Voluntary Carbon Market in Review by MSCI

13) VCM 2023 Review by Climate Focus

14) Paying for Quality State of the Voluntary Carbon Markets 2023 by Ecosystem Marketplace

15) Meta committed a pre-order of 6.75 Mt of carbon removal credits in partnership with Aspiration

16) Mitsui invests in RRG Nature Based Solutions, a regenerative agriculture project developing company in US

17) Microsoft Signs One of the Largest-Ever Nature-Based Deals to Remove 1.5 Million Tons of Carbon

18) Amazon to make initial investment of $3 mn in nature-based projects in India

19) Apple expands innovative Restore Fund for carbon removal

20) Lombard Odier Investment Managers and Systemiq announce holistiQ Investment Partners

21) Leading Global NGOs Launch SCeNe Coalition to Deliver Nature-based Climate Solutions in Southeast Asia

22) Ardian and aDryada announce the launch of Averrhoa Nature-Based Solutions, a strategy dedicated to large-scale nature-based projects